Many managers have their hands tied by strict corporate HR bands and budget freezes. If your boss literally cannot give you the cash you need to offset inflation, you must negotiate for alternative compensation that lowers your living costs.

The most valuable alternative is Remote Work.

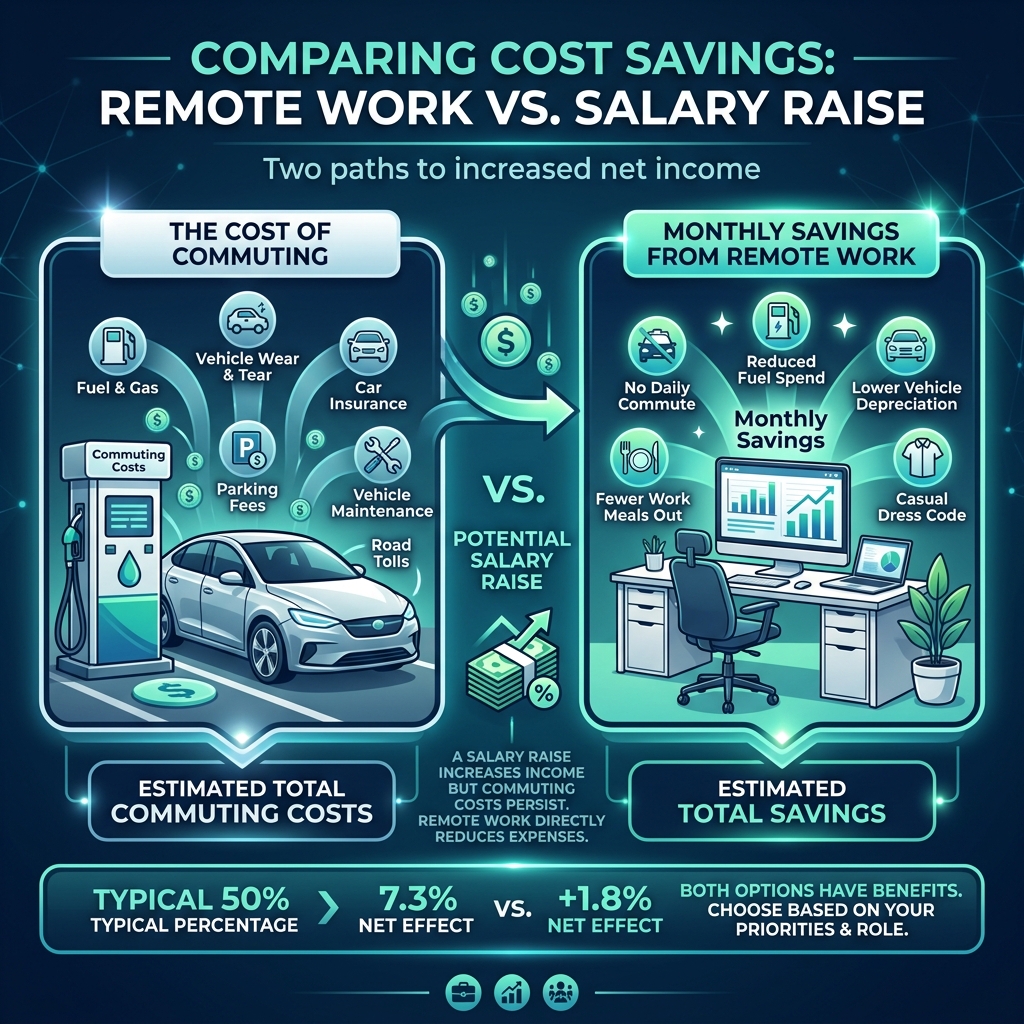

Commuting is incredibly expensive. Between fuel, tolls, parking, and transit passes, the average commuter spends thousands of dollars a year just getting to the office. If your employer refuses a 5% raise, ask to work from home two extra days a week. Use the Commuting Cost Calculator to show how much money you will save. For many suburban workers, cutting out a long commute two days a week puts just as much real wealth back into their budget as a traditional raise.

Other valuable alternatives to negotiate include: - Increased employer matches for your 401(k) or health savings accounts. - Additional Paid Time Off (PTO). - Home office stipends to cover internet and phone bills. - Professional development budgets (certifications or courses).

If your employer refuses to adjust your salary for inflation and refuses to offer cost-saving alternatives, they are silently asking you to finance their stagnant budgets with your declining living standards. At that point, the most effective negotiation strategy is finding a new job that pays exactly what you are worth.

Quick-Reference: Alternative Compensation Values

| Alternative |

Typical Annual Value |

Difficulty to Negotiate |

| Remote Work (2 days/week) |

$3,000 - $6,000 |

Medium |

| Increased 401(k) Match |

$1,000 - $3,000 |

Easy |

| Extra PTO (5 days) |

$1,500 - $3,000 |

Medium |

| Home Office Stipend |

$500 - $1,500 |

Easy |

| Professional Development |

$1,000 - $5,000 |

Easy |

Use this table as a cheat sheet during your negotiation. If a cash COLA is off the table, pivot to the alternatives with the highest annual value and the lowest negotiation difficulty. Stacking two or three of these can easily offset a $2,000 to $5,000 inflation gap.