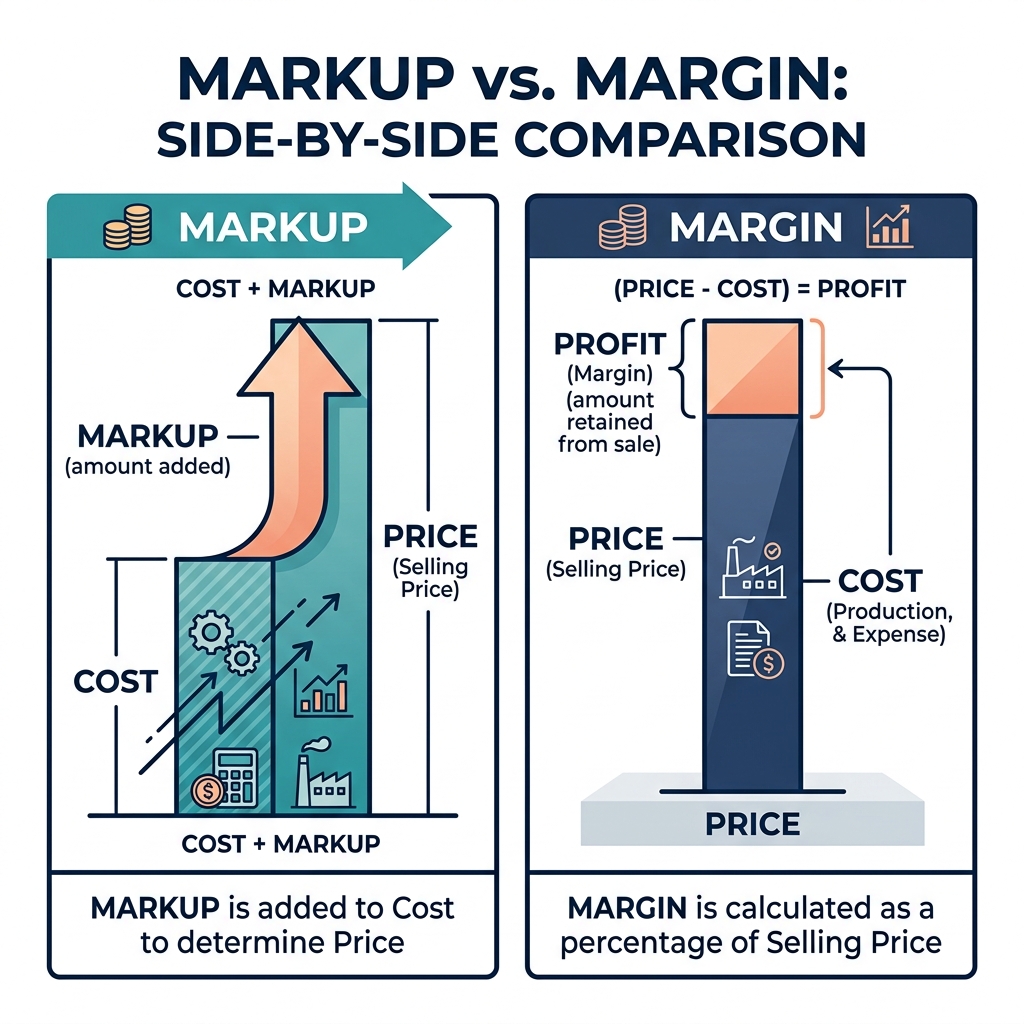

Quick Answer: The Difference Between Markup and Margin

The difference between markup and margin is what each percentage is calculated against. Markup is profit divided by cost (how much you added on top of cost). Margin is profit divided by selling price (what share of revenue is profit). The same transaction produces two different numbers: a product with a $60 cost sold for $100 has a 66.7% markup but a 40% margin.

The Core Formulas at a Glance

| Term | Formula | $60 cost, $100 price | Result |

|---|---|---|---|

| Markup | Profit / Cost | $40 / $60 | 66.7% |

| Margin | Profit / Selling Price | $40 / $100 | 40.0% |

The 30-second rule: A 50% markup equals a 33.3% margin. The conversion formula is Margin = Markup / (1 + Markup). Scroll down for a full conversion table covering 10% through 400% markup.

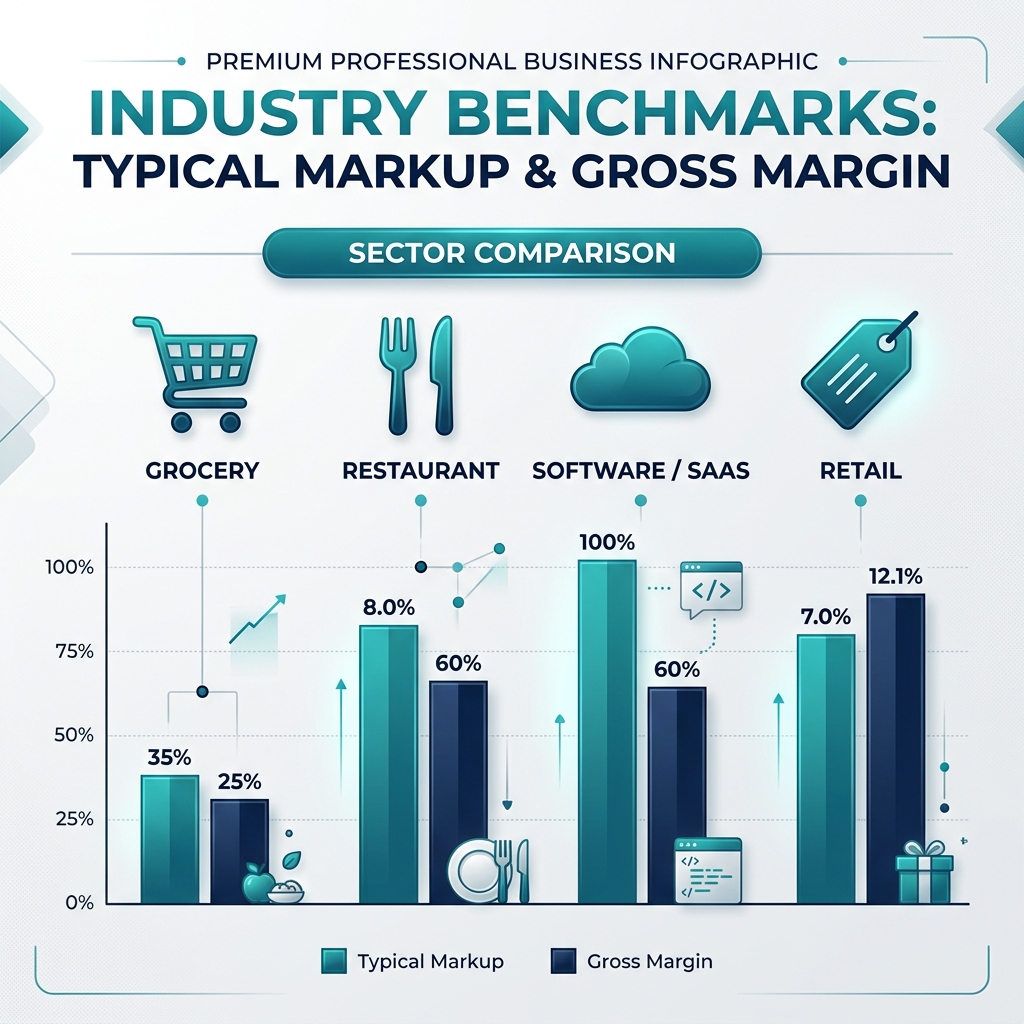

For step-by-step examples and industry benchmarks, keep reading. To verify your numbers right now, use the Markup Calculator or Profit Margin Calculator.