How US and German Tax Systems Differ: A Quick Overview

The United States and Germany represent two fundamentally different philosophies of taxation and social welfare. The US operates a lower-tax, higher-individual-responsibility model, while Germany uses a high-tax, high-social-safety-net model designed to provide comprehensive cradle-to-grave security.

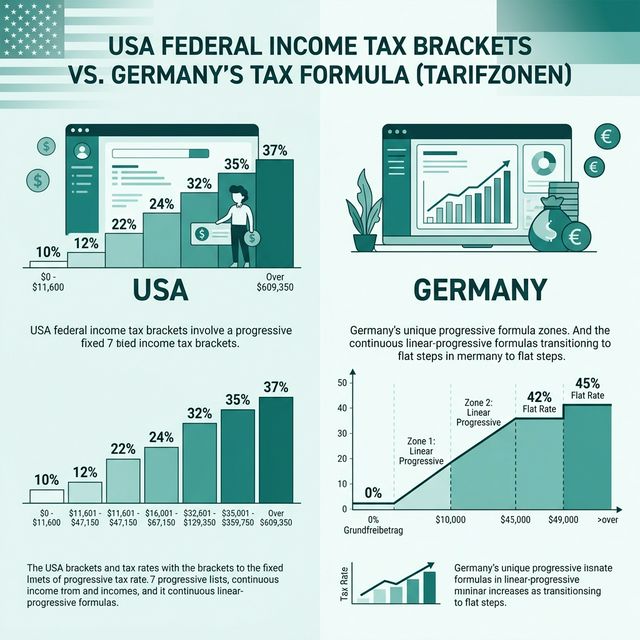

Both countries use progressive income taxation, but the rates and thresholds diverge sharply. Germany's system is famous for its 'tax progression' where rates rise continuously with income rather than jumping in discrete steps like the US federal brackets. Additionally, Germany adds several layers unknown in the US, such as Church Tax (Kirchensteuer) and the Solidarity Surcharge (Solidaritätszuschlag).

The difference in social contributions is equally stark. German workers contribute heavily to a mandatory social insurance system (Sozialversicherung) covering health, long-term care, pensions, and unemployment. In exchange, they face almost no out-of-pocket costs for healthcare or higher education. US workers pay lower payroll taxes (FICA) but must often fund their own health insurance, retirement savings (401k), and children's education.

On consumption, Germany's 19% VAT is a substantial part of the tax burden, compared to the much lower (and geographically varying) sales tax in the US.

This guide breaks down every layer of both systems with up-to-date 2024 and 2025 data.