How US and Indian Tax Systems Differ: A Quick Overview

Comparing the US and Indian tax systems requires understanding the very different economic contexts in which they operate. India has the world's fifth-largest economy by GDP but a per-capita income that is a fraction of the US level. The tax systems reflect these structural differences, with India relying more heavily on indirect taxes and compulsory savings mechanisms.

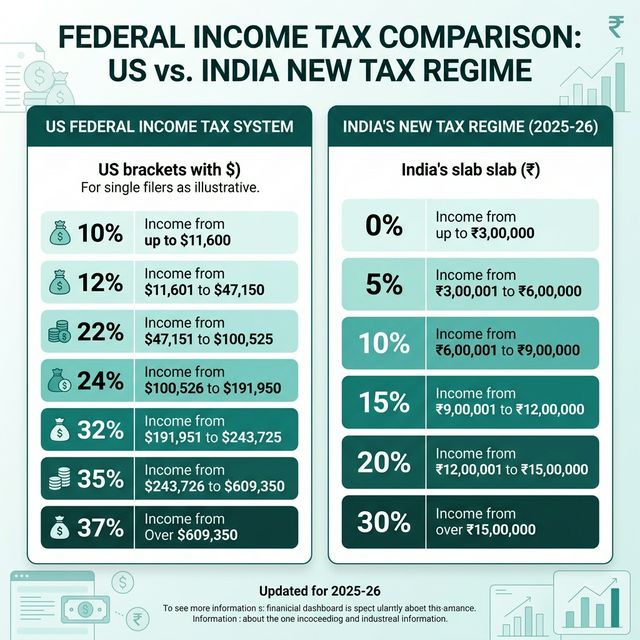

Both countries use progressive income tax, but the structures are very different. The US federal system has seven brackets with rates from 10% to 37%, while India recently simplified its structure through a new tax regime introduced in FY 2023-24. Under India's new regime (now the default), there are six slabs from 0% to 30%, but crucially, a full rebate under Section 87A exempts income up to INR 12 lakh from any tax.

India also operates an old tax regime with higher rates but more deductions (80C, 80D, HRA, LTA, etc.). Workers can choose between the two regimes annually, making the comparison more complex than a simple rate table.

On consumption taxes, India uses a Goods and Services Tax (GST) with multiple rates (0%, 5%, 12%, 18%, 28%), unlike Australia's clean 10% single rate or the US's state-by-state patchwork system. The highest 28% slab applies to luxury and demerit goods.

Retirement savings are handled through the Employee Provident Fund (EPF), a mandatory scheme where both employees and employers contribute 12% of basic salary, with the employee contribution reducing take-home pay. The US relies on voluntary 401(k) plans plus Social Security.

Health insurance is another critical difference. India has a large public health infrastructure that is free or subsidised for many residents, though quality varies dramatically by location and institution. The US private health insurance system involves significant out-of-pocket costs even for insured workers.

This guide compares both systems at realistic salary levels for Indian and US professionals.