How US and UK Tax Systems Differ: A Quick Overview

The United States and the United Kingdom share a language and a long economic relationship, but their tax systems are structured very differently. Understanding these differences is essential for professionals considering international relocation, remote workers operating across borders, or anyone trying to compare living standards between the two countries.

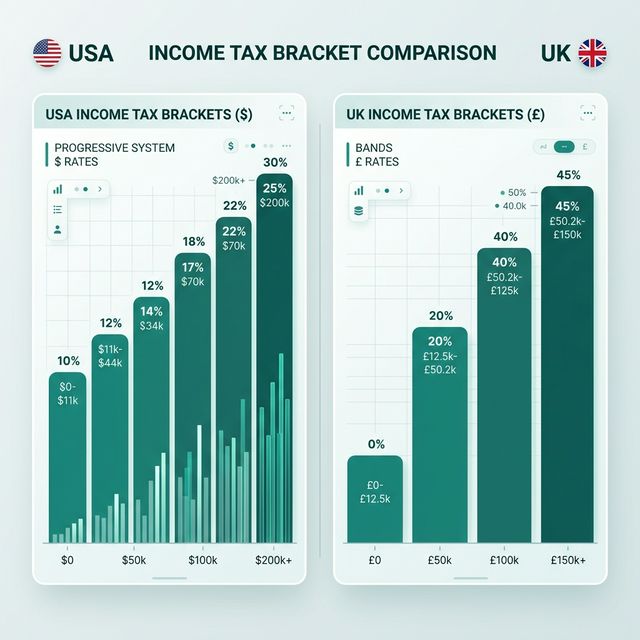

Both countries use progressive income tax systems, but the rates, thresholds, and supplementary layers diverge significantly. The US system has a federal income tax layer combined with a separate state income tax in most states, creating a two-tier structure where your total rate depends heavily on where you live. The UK uses a unified PAYE (Pay As You Earn) system administered nationally, with no equivalent regional income tax for most residents.

On consumption taxes, the UK operates a simple and uniform Value Added Tax (VAT) of 20% that applies nationwide. The US has no federal sales tax and instead relies on a patchwork of state and local taxes that vary from 0% to over 11% depending on jurisdiction.

Payroll contributions also differ fundamentally. UK workers pay National Insurance Contributions (NICs), while US workers pay FICA (Federal Insurance Contributions Act) taxes covering Social Security and Medicare. The rates are comparable, but the benefits, thresholds, and structures vary.

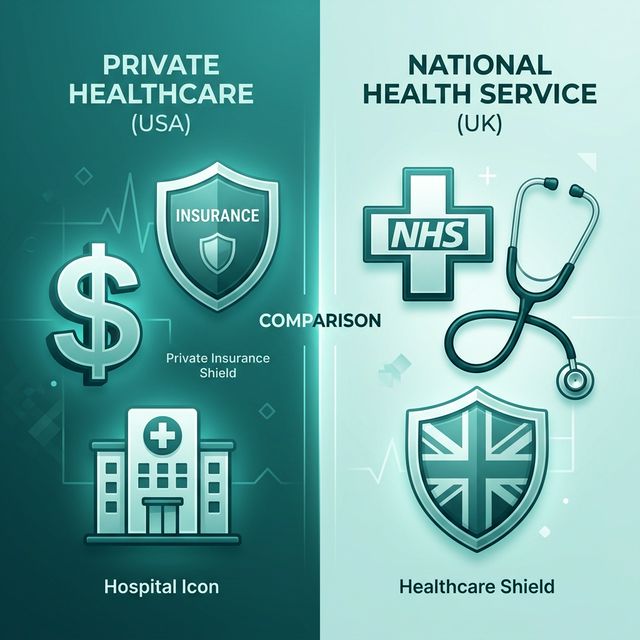

Perhaps the most discussed difference is healthcare. The UK funds the National Health Service (NHS) through general taxation, providing free-at-point-of-use care for residents. American workers typically pay thousands per year in private health insurance premiums on top of their taxes.

This guide breaks down every layer of the comparison with real 2025 numbers.